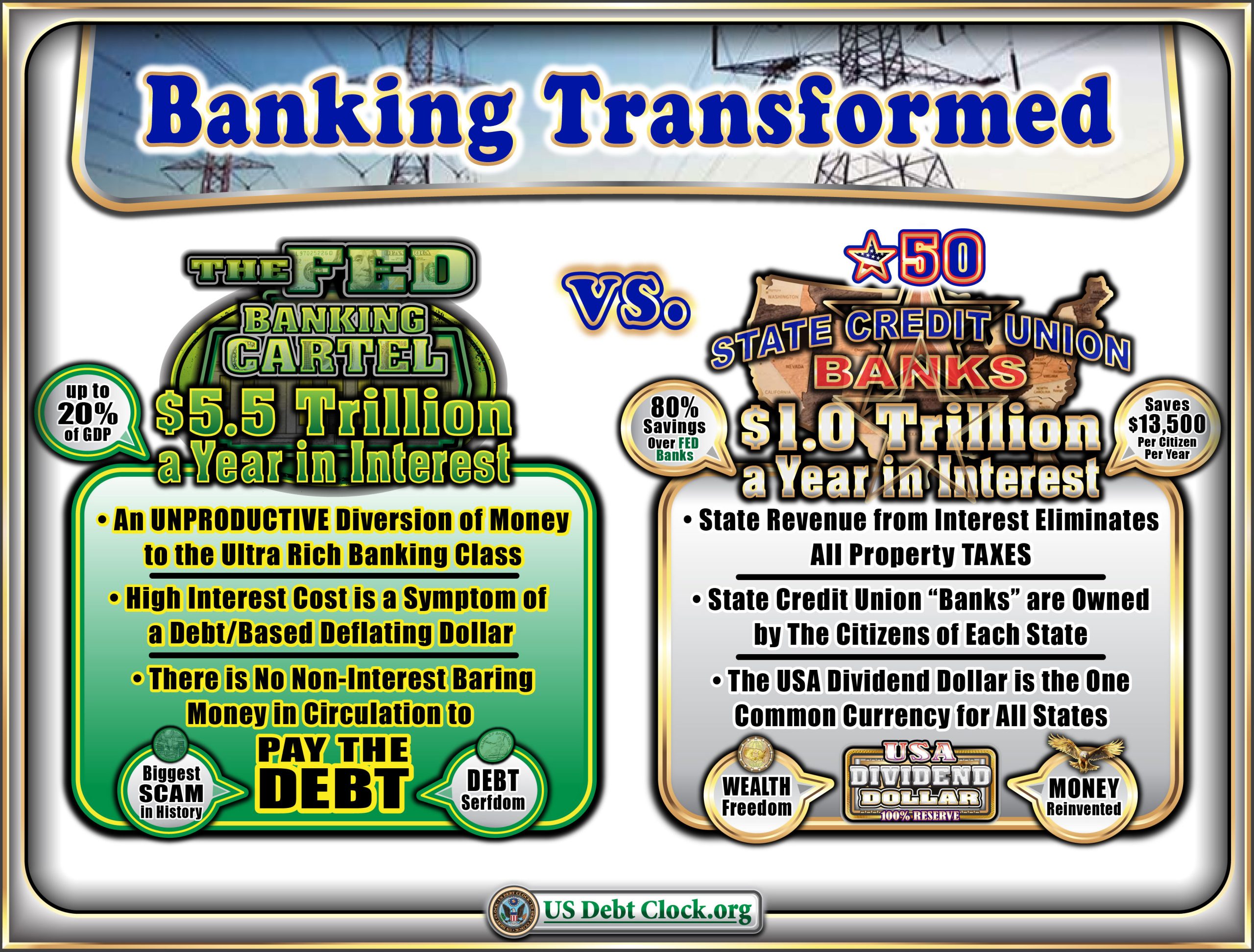

The March 12, 2026 US Debt Clock poster titled “Banking Transformed” is a split-screen argument in picture form. On the left, it depicts “The Fed / Banking Cartel” extracting $5.5 trillion a year in interest (with callouts like “debt serfdom” and “biggest scam in history”). On the right, it proposes an alternative: “50 State Credit Union Banks” generating $1.0 trillion a year in interest, “owned by the citizens,” with savings claims like “$13,500 per citizen per year,” and even the idea that state interest revenue could eliminate property taxes.

At the bottom, the poster anchors its “new system” idea to a single, common currency label: the “USA Dividend Dollar” (100% reserve).

As always: this is not an official Treasury policy document. It’s a symbolic thesis about how banking could be redesigned, and why the old architecture frustrates so many people.

Let’s decode the message—and then get practical about what it could mean for offshore banks if anything resembling this direction gained traction.

What the poster is really arguing

1) The old system is “interest extraction”

The left panel’s core claim is that the current regime routes a massive share of national income to the financial sector through interest—especially when money is created as credit and the economy must constantly service expanding debt. It frames this as unproductive diversion to an “ultra-rich banking class.”

Whether you agree with the rhetoric or not, the emotional point is clear:

The public experiences banking as a toll booth.

2) The alternative is “public-benefit credit”

The right panel flips the concept: instead of private banking franchises capturing the spread, the poster imagines state-level, citizen-owned credit institutions capturing it—then recycling that revenue back to residents (directly or through reduced taxes).

In plain English, it’s proposing a “public utility” model for money and credit:

- credit creation is treated as infrastructure,

- the “profit” from banking becomes public revenue,

- and a national “Dividend Dollar” becomes the settlement layer everyone uses.

3) The “Dividend Dollar” is the new settlement story

The poster’s bottom line is not just about banks; it’s about money design. “Dividend Dollar” suggests a currency that carries distribution features (or at least public participation) instead of functioning purely as a debt-based unit.

If banking were “transformed” like this, what changes?

Even if this remains symbolic, the poster implies five big shifts:

- Lower tolerance for high interest burdens (political pressure to reduce the cost of money).

- More public-sector involvement in retail credit (especially mortgages and consumer lending).

- More scrutiny of private banking spreads and fees (less patience for “rent seeking”).

- A move toward simpler, more transparent money (the “100% reserve” vibe).

- Distribution mechanisms becoming normal policy tools (dividends, rebates, credits).

Those shifts are exactly where offshore banking comes into the conversation.

How this could affect offshore banks

Offshore banks don’t exist in a vacuum. They live on correspondent networks, regulatory credibility, and cross-border trust. A major rethink of U.S. banking/settlement—real or rumored—would ripple outward in several ways.

1) Deposit flows could become more “barbell”

If onshore banking becomes more “public utility” and retail-friendly, some clients may feel less need to go offshore for stability.

At the same time, if the transition feels politically contentious or uncertain, you may see more offshore diversification from:

- high-net-worth families,

- internationally mobile entrepreneurs,

- and companies hedging jurisdiction risk.

So offshore banks could see both:

- inflows from “uncertainty hedgers,” and

- outflows from clients who simply wanted better retail banking and can now get it domestically.

2) Offshore banking’s value proposition shifts from secrecy to services

This is already happening, and a “Banking Transformed” narrative accelerates it.

Offshore banks that win in the next decade will look less like “hiding places” and more like:

- multicurrency treasury managers,

- cross-border structuring partners,

- trade and commodities facilitators,

- custody/wealth administration platforms,

- and jurisdictional diversification experts.

In other words: compliance-forward, solutions-forward.

3) Correspondent banking becomes even more important (and more selective)

If U.S. banking gets reorganized—or even if markets expect it—correspondent banks tend to tighten:

- more de-risking,

- more documentation,

- more pressure on smaller offshore institutions.

That usually favors:

- well-capitalized offshore banks,

- strong KYC/AML programs,

- clean audit trails,

- and jurisdictions with credible regulators.

4) FX and settlement rails could become volatile during “switch talk”

Even without an official switch, narratives can move markets.

If traders think a new settlement framework is coming, offshore banks will feel it through:

- widened spreads in certain currency pairs,

- increased hedging demand,

- more client questions about “which dollars” (and which rails),

- and higher operational demands for fast settlement and liquidity.

The offshore winners will be the banks that can deliver speed, clarity, and liquidity across multiple rails.

5) Tax and reporting pressure doesn’t disappear—it intensifies

A system that claims to “return banking benefits to citizens” will likely come with stronger “fairness” messaging. That often pairs with:

- tougher enforcement,

- greater transparency expectations,

- and louder political narratives about “closing loopholes.”

For offshore banks, that means the trendline is the same:

transparent, documented, compliant cross-border banking survives; gray-zone banking gets squeezed.

The practical takeaway for Invest Offshore readers

Whether the US Debt Clock poster is prophecy or persuasion, it’s pointing at a real global direction:

Banking is being re-legitimized as public infrastructure, and money is being re-imagined as a system feature—not just a bank product.

If that direction accelerates, offshore banks won’t vanish—but they will evolve:

- less “offshore for secrecy,”

- more “offshore for diversification, multicurrency access, global custody, and cross-border execution.”

And the offshore institutions best positioned will be the ones that can say, with receipts:

“We’re not outside the system. We’re built to operate cleanly across it.”

Invest Offshore continues to track real-asset opportunities globally, including investment opportunities in West Africa seeking investors for the Copperbelt Region, plus verified gold for sale through our network and partners worldwide, and select mining concessions with documented title, geology, and clear pathways to production.

Leave a Reply