The world’s dominant financial messaging network is borrowing the architecture of crypto while keeping regulated banks firmly in control

The dividing line between traditional banking and digital assets just became considerably harder to see.

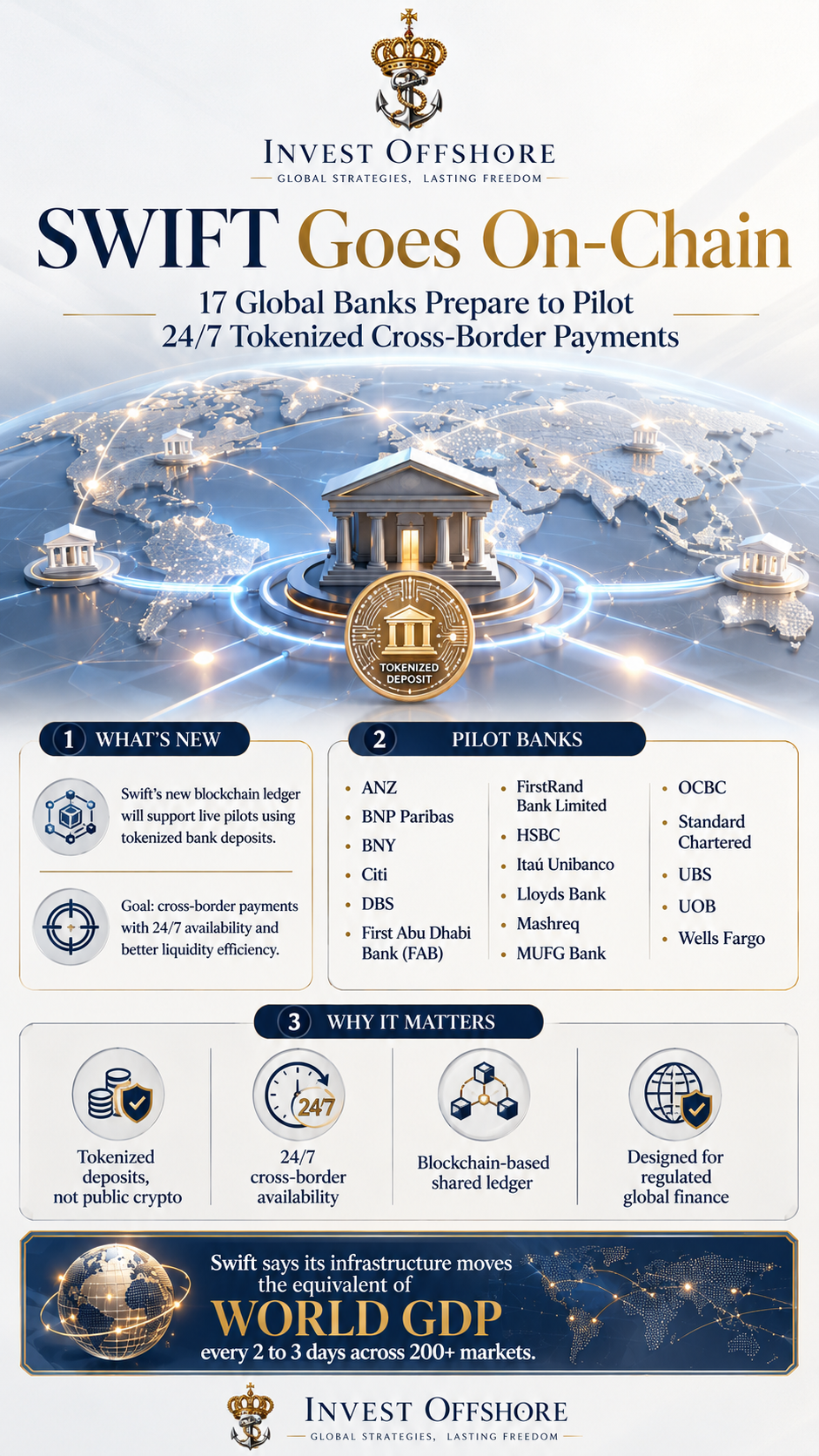

On July 9, 2026, SWIFT announced that its new blockchain-based ledger is ready for initial use. Seventeen major banks spanning six continents are now preparing to pilot live cross-border transactions using tokenized commercial-bank deposits.

The objective is straightforward but potentially transformative: allow regulated banks to move value across borders around the clock—including nights, weekends and holidays—without abandoning the compliance, credit controls and settlement infrastructure on which the international banking system depends. (Swift)

This is not SWIFT surrendering to crypto.

It is SWIFT absorbing some of crypto’s most valuable characteristics.

From Banking Hours to Always-On Money

Traditional international payments are constrained by operating hours, time zones, correspondent-bank processes and the availability of domestic settlement systems.

Digital assets changed expectations by demonstrating that value could move globally at any hour. Corporate treasurers, financial institutions and international investors increasingly expect conventional money to offer the same availability.

SWIFT’s answer is a shared blockchain ledger that acts as a secure coordination—or orchestration—layer between participating banks.

Each bank can issue tokenized representations of its deposits on its own controlled ledger. SWIFT’s shared infrastructure then records and validates the commitments between institutions, providing them with a synchronized view of the payment as it moves through the process.

Funds can therefore be initiated and coordinated overnight or during weekends, while final settlement is still completed through established banking systems. Existing compliance, liquidity, credit, risk and operational controls remain in place. (Swift)

That combination matters.

It introduces the speed and continuous availability associated with crypto without requiring banks to transfer customer funds through an unregulated public token.

The 17 Banks Preparing for Live Pilots

The initial participants represent nearly every important banking region:

- ANZ

- BNP Paribas

- BNY

- Citi

- DBS

- First Abu Dhabi Bank

- FirstRand Bank Limited

- HSBC

- Itaú Unibanco

- Lloyds Bank

- Mashreq

- MUFG Bank

- OCBC

- Standard Chartered

- UBS

- UOB

- Wells Fargo

The group includes institutions from North America, Europe, Asia, the Middle East, Africa, Australia and South America. That geographic diversity suggests SWIFT is not building a narrow regional experiment. It is testing whether tokenized commercial-bank money can operate across the existing international banking network. (Swift)

SWIFT says the ledger went from concept to activation in approximately nine months, following development shaped by international financial institutions. The controlled initial launch is expected to expand in both functionality and availability as participating banks gain experience with live transactions. (Swift)

Crypto-Style Does Not Mean Cryptocurrency

The language surrounding this development requires precision.

A tokenized deposit is not necessarily a stablecoin such as USDC or USDT. It is a digital representation of money held as a liability of a regulated commercial bank.

The distinction affects everything from redemption rights and balance-sheet treatment to compliance, deposit protection, counterparty risk and regulatory oversight.

With a tokenized bank deposit:

- The issuing bank remains responsible for the underlying deposit.

- Customer identification and anti-money-laundering controls remain within the banking system.

- The tokens operate inside permissioned institutional environments.

- Banks retain control over their keys, assets, liquidity and settlement arrangements.

- Final settlement may still occur through real-time gross settlement systems, correspondent accounts or other agreed banking mechanisms.

In other words, the technology may resemble crypto, but the legal and institutional framework remains unmistakably bank-based.

SWIFT will operate the shared ledger and coordinate transaction workflows, while participating banks maintain authority over their own environments. (Swift)

Built on Ethereum-Compatible Infrastructure

The technical architecture is also revealing.

SWIFT previously disclosed that the minimum viable product uses an Ethereum Virtual Machine-compatible design based on Hyperledger Besu, an open-source enterprise blockchain platform.

That architecture gives the ledger familiarity with the broader digital-asset ecosystem while remaining suitable for permissioned institutional use. It may also make future interoperability with tokenized securities, regulated stablecoins, central-bank money and other blockchain networks easier to develop. (Swift)

The ledger is therefore more than a faster payment channel.

It could become a connective layer through which different forms of regulated digital value are coordinated across institutions and jurisdictions.

Potential future applications identified by SWIFT include programmable corporate payments, payment-versus-payment foreign-exchange transactions and cash movements connected to securities settlement. The organization has also highlighted longer-term possibilities involving programmable money and agent-driven commerce. (Swift)

SWIFT Is Not Being Replaced—It Is Reinventing Itself

For years, crypto advocates predicted that blockchain networks would make SWIFT obsolete.

The reality may prove more nuanced.

SWIFT already connects more than 11,500 institutions and operates across more than 200 countries and territories. It supports over 40,000 payment routes, while value equivalent to the world’s gross domestic product passes across its network roughly every three days. (Swift)

That reach cannot be recreated quickly.

Rather than allow new digital networks to fragment global liquidity, SWIFT is inserting blockchain technology into infrastructure banks already know, trust and use.

It is also important to recognize that today’s SWIFT network is faster than its reputation sometimes suggests. SWIFT reports that 75% of payments reach the beneficiary bank within ten minutes, frequently within seconds. The remaining friction often occurs during the final stage, when the receiving institution must complete compliance checks, apply local processing procedures and credit the beneficiary’s account. (Swift)

The blockchain ledger is intended to improve coordination and eliminate artificial operating cutoffs—not simply repair a network on which every payment takes several days.

Why This Matters for Offshore Finance

For international companies, private banks, investment structures and offshore treasury operations, the principal benefit could be liquidity efficiency.

A business operating across New York, London, Dubai, Singapore and Hong Kong should not have to manage its money according to the business hours of a single financial center.

Always-on tokenized deposits could eventually allow institutions to:

- Move liquidity between banking regions outside conventional operating hours.

- Respond more quickly to margin calls and collateral requirements.

- Improve real-time visibility over international cash positions.

- Reduce funds left idle as protection against settlement uncertainty.

- Coordinate foreign-exchange transactions more efficiently.

- Connect tokenized securities with tokenized cash for faster settlement.

These benefits will not appear everywhere immediately. The initial phase is a controlled pilot, and the commercial terms, currencies, corridors and transaction volumes have not yet been fully disclosed.

Nevertheless, the direction is clear.

The international banking system is preparing for a world in which money, securities and collateral operate on shared digital ledgers continuously rather than only during traditional market hours.

Banks Are Building Their Answer to Stablecoins

Stablecoins exposed a genuine weakness in the legacy financial system: global businesses operate 24 hours a day, but bank money often does not.

SWIFT’s ledger represents an institutional response.

Instead of asking corporations to move liquidity outside the banking system, banks can tokenize their own deposits and offer many of the same functional advantages—instant availability, programmability, shared records and cross-border portability—inside a regulated structure.

The competition ahead may therefore be less about “banks versus blockchain” and more about which form of blockchain money gains the greatest adoption:

- Public stablecoins

- Bank-issued tokenized deposits

- Wholesale central-bank digital currency

- Tokenized money-market instruments

- Hybrid networks connecting several forms of regulated value

SWIFT appears determined to support interoperability among these emerging forms rather than betting the future on a single digital currency.

The Great Financial Convergence

The significance of this announcement extends beyond one payment pilot.

Seventeen globally significant banks are preparing to conduct live transactions using tokenized deposits on blockchain infrastructure operated by the institution at the center of conventional cross-border finance.

That is convergence in plain sight.

Crypto introduced the concept of programmable, always-available digital value. The banking system is now adapting those ideas to regulated deposits, established legal rights and institutional-grade controls.

SWIFT is not becoming a cryptocurrency network.

It is doing something potentially more consequential: transforming blockchain from an alternative to global banking into part of global banking itself.

For offshore investors and international businesses, the message is unmistakable.

The financial system is moving on-chain—and this time, banks are coming with it.

Leave a Reply